Home Legal Services Company / Corporate

Expert legal advice for businesses raising investment and investors putting money into private companies.

Whether you’re a growing business looking to raise capital or an investor considering putting money into a private company, getting the legal side right is crucial. The wrong investment structure can cost you tax relief, dilute your ownership more than necessary, or leave you without the protections you need.

Our investment solicitors work with businesses and investors across all types of funding rounds, from angel and seed investment through to venture capital and private equity deals. We’ll help you structure the transaction, negotiate the terms, and make sure the paperwork protects your interests.

Get a free, no-obligation chat with our corporate and commercial team, call us on 02920 829 100 or use our Contact us form.

Excellent rating by Review Solicitors | Ranked in Legal 500 and Chambers & Partners.

Every investment is a balancing act. Investors want protections that minimise their risk and maximise their potential returns. Businesses want capital without giving away too much control or setting terms they’ll regret later.

Getting this balance right requires careful thought about structure, valuation, governance, and the specific terms of the deal. It also requires documentation that clearly sets out what everyone’s agreed, so there are no nasty surprises down the line.

We’ve advised on investment transactions of all sizes, from founders raising their first £50,000 from friends and family to multi-million pound venture capital rounds. Whatever your situation, we’ll give you practical, commercial advice that helps you get the deal done on terms that work.

If you’re thinking about raising investment or investing in a private company, let’s have a conversation about your options.

Get a free, no-obligation chat with our corporate and commercial team, call us on 02920 829 100 or use our Contact us form.

Raising external investment is a significant step for any business. You’re bringing in new shareholders who’ll have a stake in your company’s future, and often a say in how it’s run. Getting the legal framework right from the start saves problems later.

Early-stage funding from angel investors, friends and family, or seed funds is often a company’s first experience of external investment. The amounts might be smaller, but the legal considerations are just as important.

We can help you with:

VC funding rounds involve more complex negotiations and documentation. Investors will expect certain standard protections, but there’s usually room to negotiate terms that work for both sides.

We can help you with:

PE transactions typically involve larger sums and more sophisticated investors. The documentation is more extensive and the negotiations more intensive, but the fundamental principles are the same.

We can help you with:

Sometimes it makes sense to take investment now and convert it to equity later, often at a discount to the next funding round. Convertible loan notes can achieve this.

We can help you with:

Investing in a private company means putting your money at risk. Unlike public markets, there’s no easy way to sell your shares if things don’t work out. Proper due diligence and strong contractual protections are essential.

If you’re investing your own money in early-stage companies, you need to understand what you’re getting and make sure your investment is properly documented.

We can help you with:

Investing alongside other angels? We can help structure the arrangement and make sure everyone’s interests are aligned.

We can help you with:

Already invested and considering putting more money in? We’ll help you understand how the new round affects your existing position and whether the terms are fair.

We can help you with:

Investment transactions involve several interconnected documents. Here’s what each one does:

The term sheet sets out the key commercial terms of the deal before detailed legal documents are prepared. It typically covers valuation, investment amount, share class, key investor rights, and the proposed timeline. Most provisions are non-binding, though confidentiality and exclusivity clauses usually are.

Getting the term sheet right saves time and money later. If fundamental issues aren’t agreed at this stage, they’ll cause problems when lawyers start drafting.

This is the main contract governing the investment. It sets out who’s investing, how much, what shares they’re getting, and the conditions that need to be satisfied before completion.

Key provisions include warranties from the company and founders, conditions to completion, and the mechanics of how shares are issued and paid for.

The shareholders’ agreement governs the ongoing relationship between shareholders after the investment completes. It covers matters like board composition, reserved matters requiring investor consent, information rights, dividend policy, transfer restrictions, and what happens on exit.

Unlike articles of association, shareholders’ agreements are confidential and can be tailored to the specific needs of the parties.

The articles are the company’s constitutional document and are publicly available at Companies House. They set out the rights attached to different share classes, how decisions are made, and the mechanics of share transfers.

Investment rounds often require amendments to the articles to create new share classes or implement specific provisions.

In most investment transactions, the company and founders give warranties about the state of the business. The disclosure letter qualifies those warranties by setting out known issues. If something is properly disclosed, the investor can’t claim for breach of warranty on that point.

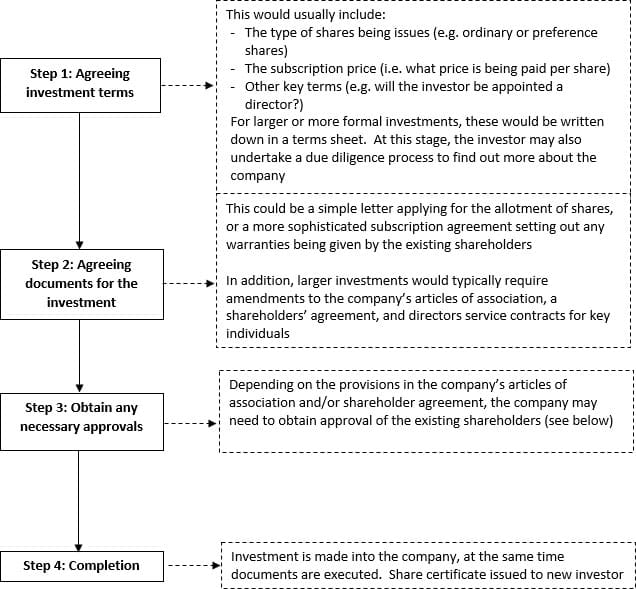

While every deal is different, most investment transactions follow a similar path:

Stage 1: Initial Discussions and Term Sheet

The company and potential investors discuss the opportunity and negotiate key terms. If they reach agreement in principle, this is documented in a term sheet or heads of terms. At this stage, it’s worth getting legal input to make sure the terms are workable and you haven’t missed anything important.

Stage 2: Due Diligence

Investors investigate the company to verify what they’ve been told and identify any risks. The scope depends on the deal size and investor sophistication. For angel rounds, this might be relatively light. For VC/PE deals, it’s typically more extensive.

Stage 3: Documentation

Lawyers prepare the investment agreement, shareholders’ agreement, and any other documents needed. These are negotiated between the parties, often with several rounds of comments and discussions.

Stage 4: Disclosure

The company prepares a disclosure letter setting out anything that qualifies the warranties in the investment agreement. This is an important step that protects founders from warranty claims.

Stage 5: Completion

Once all conditions are satisfied and documents agreed, the parties sign, money is transferred, and shares are issued. The company’s registers are updated and filings made at Companies House.

Stage 6: Post-Completion

After completion, there’s admin to handle, including updating statutory registers and issuing share certificates.

Investors typically seek certain rights to protect their position. Here are some of the most common:

Investors often want a seat on the board, or at least the right to appoint a board observer. This gives them visibility of what’s happening and influence over key decisions.

Certain significant decisions may require investor consent, such as issuing new shares, taking on debt, making major acquisitions, changing the business, or paying dividends. The list is negotiable, but investors will want protection on matters that could affect their investment.

Investors typically receive regular financial and operational updates. This might include monthly management accounts, annual audited accounts, and notification of material events.

If the company raises money at a lower valuation in future (a “down round”), anti-dilution provisions can protect earlier investors from excessive dilution. The most common mechanisms are weighted average and full ratchet anti-dilution.

Pre-emption gives existing shareholders the right to participate in future funding rounds to maintain their percentage ownership. Without this, investors can be diluted by subsequent rounds.

Tag-along rights let minority shareholders sell alongside a majority shareholder who’s selling. Drag-along rights let a majority force minorities to sell, typically to facilitate a clean exit.

On a sale or winding up, investors with liquidation preferences get paid before ordinary shareholders, up to a specified multiple of their investment. This protects investors if the exit value is less than hoped.

Choosing a law firm is a big decision. You want experts who actually get you and your organisation, respond when you need them, and give you straight answers. That’s us. We’re one of Wales’ leading commercial law firms, and we do things a little differently.

You won’t be passed through layers of gatekeepers here. When you call, you’ll speak to the solicitor handling your matter. You’ll have their direct dial, their email, and a genuine working relationship. Our clients tell us this makes all the difference when deals move quickly and decisions need to be made.

We don’t work in silos. Our corporate team works closely with colleagues in employment, tax, and commercial to make sure every aspect of your transaction is covered. If your investment involves EMI share options, property, or employment matters, we’ll bring in the right people.

Devolved decision-making and flexible working hours mean we can move at pace. Investment transactions often have tight deadlines. We’re set up to respond when you need us.

You’ll always get the full picture from us. If a term sheet has problems, we’ll tell you. If an investor is asking for something unreasonable, we’ll explain why and help you push back. No sugar-coating, just practical guidance on what matters.

Investment transactions need to be cost-effective, especially for early-stage companies where every pound counts. We’ll give you a clear fee estimate at the outset and many of our services are available for fixed or capped fees.

We’re the leading commercial law firm with offices in South and North Wales offering Welsh language legal services at every level, from trainees right through to partners. This isn’t an add-on or a tick-box exercise. It’s part of who we are.

Excellent rating by Review Solicitors | Ranked in Legal 500 and Chambers & Partners.

We charge for investment work in different ways depending on the complexity:

Fixed fees – For straightforward angel rounds with standard documentation, we can often agree a fixed price upfront.

Capped fees – For more complex transactions with some variables, we may agree a fee cap so you have budget certainty.

Hourly rates – For VC/PE deals or where the scope is uncertain, we charge by the hour but keep you regularly updated on costs.

Contact us for a quote specific to your transaction.

We were delighted with the service from Darwin Gray. The service was both professional and personable; a genuine pleasure to deal with. A big thank you to the corporate team who supported us in raising our seed round. Their experience and expert advice was invaluable as we navigated a complicated deal with a number of parties, and we will be forever grateful to them for their exceptional service.

They provide sensible and pragmatic advice. Legal 500![]()

They are flexible and responsive. Legal 500![]()

An investment agreement is a legal contract that sets out the terms on which someone invests money in a company. It covers who’s investing, how much, what type of shares they’re getting, the price, and the conditions that must be met before the investment completes. It also includes warranties from the company about its current state and protections for the investor. The agreement works alongside a shareholders’ agreement, which governs the ongoing relationship between shareholders after the investment.

To invest in a private company, you’ll typically need to find an investment opportunity (through your network, angel groups, or crowdfunding platforms), conduct due diligence on the company, negotiate terms, and complete the legal documentation. Unlike public companies, you can’t simply buy shares on a stock exchange. You’ll need to subscribe for new shares or buy existing shares from a current shareholder. Most investments are documented through a subscription agreement and shareholders’ agreement.

A seed investment agreement is the legal documentation for an early-stage funding round, typically the first external investment a company receives. It’s usually simpler than documentation for later-stage VC rounds, but covers the same core elements: who’s investing, how much, what shares they get, key terms and protections, and the conditions for completion.

Investor rights are negotiable, but commonly include: board representation or observer rights; consent rights over significant decisions (reserved matters); information rights to receive regular financial updates; pre-emption rights to participate in future funding rounds; anti-dilution protection if the company raises money at a lower valuation; tag-along rights to sell alongside other shareholders; and liquidation preferences that prioritise investors on exit. The specific rights depend on the size of investment, the investor’s bargaining power, and market norms for the type of deal.

While there’s no legal requirement, professional advice is strongly recommended for both companies and investors. For companies, getting the structure wrong can have serious consequences, setting terms you’ll regret in future rounds. For investors, you’re putting money at risk and need to understand what you’re getting and what protections you have. The cost of legal advice is usually modest compared to the amounts being invested and the potential consequences of getting it wrong.

An ASA is a way of taking investment now while deferring the share issue until later, typically until a larger funding round. Investors pay money upfront and receive shares at a future date, usually at a discount to the price paid by investors in the next round. ASAs are popular for early-stage fundraising.

A shareholders’ agreement is a contract between the shareholders of a company (and usually the company itself) that governs their relationship. It covers matters like how the board is composed, what decisions need shareholder consent, information rights, dividend policy, restrictions on share transfers, and what happens on exit. Unlike articles of association, shareholders’ agreements are private (not filed at Companies House) and can be tailored to the specific needs of the parties. Most investment transactions include a new or updated shareholders’ agreement.

The process of investing will depend on the individual circumstances of the investment. For example, if an individual is investing in a friend or family’s business, then the process will usually be much simpler than the process a venture capitalist of angel investor would want to follow. In addition, if an investor comes through a funding platform, then the process is likely to be different again.

As a general rule of thumb, the higher the investment amount and the more experienced the investor, the more paperwork and protections they are likely to seek. An individual investing a small sum of money in a friend or family’s business is often less concerned with shareholder protections.

However, at its core, an investment would usually follow the same journey:

Timescales vary significantly. Key factors include how quickly due diligence can be completed, how aligned the parties are on terms, whether SEIS/EIS advance assurance is needed, and the availability of all parties to review and sign documents.

Founders typically give warranties about the company’s current state, including that accounts are accurate, there are no undisclosed liabilities, the company owns its intellectual property, there’s no pending litigation, all taxes have been paid, and key contracts are in good standing. The scope and detail depend on the deal size. If a warranty turns out to be untrue, investors can claim for breach of contract. The disclosure letter qualifies warranties by setting out known exceptions. Founders should review warranties carefully and disclose anything relevant.

Existing shareholders may have pre-emption rights that give them first refusal on new share issues. If they do, you’ll need their consent or waiver before issuing shares to new investors. Even without pre-emption rights, certain decisions may require shareholder approval under the company’s articles or an existing shareholders’ agreement. It’s important to check the company’s constitutional documents early in the process and get any necessary consents lined up before committing to investors.

If the company becomes insolvent, shareholders typically lose their investment. Creditors are paid first, and shareholders only receive anything if there’s money left over (which is rare). Some investment agreements include liquidation preferences that give certain investors priority over others, but these only help if there’s anything to distribute.

a: 9 Cathedral Road, Cardiff, CF11 9HA

Located in the heart of Cardiff’s business district, our head office is easily accessible by car and public transport. We can provide a Cardiff registered office address for your company.

a: Unit F12, InTec, Ffordd y Parc, Parc Menai, Bangor, LL57 4FG

Our North Wales office serves businesses and investors across the region with the same expertise and direct access to our corporate team.

We advise clients throughout Wales and across the UK. Most investment transactions can be handled remotely, so your location doesn’t limit our ability to help.

Whether you’re a business looking to raise capital or an investor considering an opportunity, we’re here to help you get the deal done on terms that work.

Contact us for a free, no-obligation chat to see if we can help you. You’ll speak directly to a corporate solicitor who can discuss your situation and explain how we might work together.

Call us on 02920 829 100 or use our Contact us form.

We aim to respond to all enquiries within one working day.

To speak to one of our experts today, please contact us on 02920 829 100 or by using our Contact Us form for a free initial chat to see how we can help.