Home Legal Services Company / Corporate

Expert legal advice for business owners selling their company across Wales and the UK.

Selling a business you’ve built is one of the most significant decisions you’ll ever make. Whether it’s a retirement exit, a strategic sale to a competitor, or handing over to your management team, you want to maximise value, minimise risk, and walk away knowing you’ve got the best possible deal.

Our business sale solicitors guide owners through every stage of the sale process. We’ll help you prepare for sale, manage buyer due diligence, negotiate terms that protect your interests, and get the transaction over the line.

Get a free, no-obligation chat with our commercial team, call us on 02920 829 100 or use our Contact us form.

Excellent rating by Review Solicitors | Ranked in Legal 500 and Chambers & Partners.

Selling a business isn’t something you do every day. For most owners, it’s a once-in-a-lifetime transaction. That means you’re dealing with unfamiliar territory while the buyer (often a trade acquirer or PE house) does this regularly.

Getting professional advice early makes a real difference. Proper preparation can increase what you get for the business. Understanding the process helps you avoid mistakes. And having experienced lawyers in your corner means you’re not outmanoeuvred by a buyer who knows all the tricks.

We’ve helped business owners across Wales and the UK sell businesses of all types and sizes. From family businesses passing to the next generation to trade sales to competitors and private equity exits, we understand what sellers need and how to protect their interests.

If you’re considering selling your business, let’s talk through your options.

Get a free, no-obligation chat with our commercial team, call us on 02920 829 100 or use our Contact us form.

We support sellers throughout the entire sale process, from initial planning right through to completion and beyond.

The time to prepare for a sale is before you have a buyer. A legal health check can identify and fix problems that might otherwise reduce your price, slow down the deal, or give buyers ammunition to chip away at the purchase price.

We can help you with:

How the sale is structured affects your tax position, your ongoing liability, and how clean your exit really is. We’ll work with you and your accountant to ensure the deal is structured in a way that works for you.

We can help you with:

Once you have a buyer, the negotiation begins. Heads of terms set the framework for the deal, and getting them right saves problems later. We help sellers negotiate fair terms from the outset.

We can help you with:

Buyers investigate thoroughly before completing. How you handle due diligence affects how the deal progresses. Poor preparation leads to delays, price chips, and deals that fall apart.

We can help you with:

The sale agreement is where the deal is documented. This is where warranties, indemnities, and liability limitations are negotiated. Getting this right protects you after completion.

We can help you with:

The disclosure letter qualifies the warranties you give in the sale agreement. Proper disclosure protects you from warranty claims. Incomplete or careless disclosure can leave you exposed.

We can help you with:

Completion involves signing documents, transferring ownership, and receiving payment. But your involvement doesn’t always end there. Earn-outs, handover periods, and warranty claims may all feature.

We can help you with:

Every sale is different, but most follow a similar path. Here’s what to expect:

Before approaching buyers or engaging with offers, get your house in order. This means:

The better prepared you are, the smoother the process and the better your outcome.

Start this 6-12 months before you want to sell if possible

You might already have a buyer in mind (a competitor, an employee, a PE house that’s approached you). If not, you’ll need to find one. This might involve business brokers, corporate finance advisers, or your own network.

At this stage, confidentiality is crucial. You don’t want staff, customers, or competitors knowing your business is for sale until you’re ready.

Once you have a serious buyer, you’ll negotiate and agree heads of terms (sometimes called a letter of intent). This sets out the key commercial terms: price, structure, payment terms, exclusivity, and timeline.

Heads of terms are usually non-binding on the commercial terms, but may include binding provisions on confidentiality, exclusivity, and costs. Getting legal input at this stage is valuable.

Typically takes 1-2 weeks

The buyer investigates your business. They’ll review financial records, contracts, employment matters, property, IP, tax, and compliance. You’ll need to provide information and answer questions.

Due diligence can be intensive. Having your documents organised and being responsive keeps the process moving. Issues that emerge may need addressing or may affect the price.

Typically takes 3-6 weeks

Lawyers draft the sale agreement, disclosure letter, and other documents. This is where the detailed terms are negotiated: warranties, indemnities, liability caps, restrictive covenants, and what happens after completion.

Expect several rounds of negotiation. The buyer will push for more protection; you’ll push for less liability. Finding the right balance is key.

Typically takes 3-6 weeks

You prepare a disclosure letter setting out everything the buyer should know that might otherwise breach a warranty. This is a critical exercise that protects you from post-completion claims.

Runs alongside documentation

Once everything is agreed, you sign the documents, transfer the shares or assets, and receive payment. For straightforward deals, this happens on the same day as signing. For more complex transactions, there may be a gap while conditions are satisfied.

The completion meeting itself typically takes a few hours to a day

After completion, there’s admin to handle and possibly ongoing obligations. You may need to:

Selling a business comes with risks. Buyers will seek protections that could leave you exposed to claims after completion. Here’s how to protect yourself:

Warranties are statements about your business that you give in the sale agreement. If a warranty turns out to be untrue, the buyer can claim damages. Common warranties cover:

To protect yourself:

Sellers should always negotiate limits on their warranty liability:

Cap on total liability – Your maximum exposure, often a percentage of the purchase price

De minimis threshold – Claims below a minimum amount are excluded (stops nuisance claims)

Basket/aggregate threshold – Claims only count once they exceed a cumulative amount

Time limits – General warranty claims must be brought within 12-24 months; tax claims often have longer periods

Exclusions – No liability for matters known to the buyer, disclosed, or covered by insurance

The disclosure letter qualifies your warranties. If you properly disclose an issue, the buyer can’t claim for breach of warranty on that point.

Disclosure is your main protection against warranty claims. Take it seriously:

Buyers will want to prevent you from competing after the sale. You’ll typically be restricted from:

These restrictions need to be reasonable in scope and duration to be enforceable. Negotiate the shortest period and narrowest scope that the buyer will accept. Ensure you can still earn a living and pursue future opportunities.

If part of the price depends on future performance (an earn-out), you need to be careful about:

Earn-outs are a common source of post-completion disputes. Clear drafting and realistic expectations are essential.

Sellers can make mistakes that cost them money or leave them exposed. Here are some to avoid:

Rushing to sell often means leaving money on the table. Problems discovered during due diligence give buyers ammunition to reduce the price. Time pressure weakens your negotiating position.

Start preparing at least 6-12 months before you want to sell. Fix problems while you have time.

News that your business is for sale can worry staff, unsettle customers, and alert competitors. Ensure proper confidentiality agreements are in place before sharing sensitive information with potential buyers.

Lock-out periods give buyers exclusive access to negotiate with you. While some exclusivity is normal, giving too long or too broad an exclusivity weakens your position. Negotiate reasonable time limits and clear conditions.

Disorganised records and slow responses frustrate buyers and delay deals. Deals die when they lose momentum. Have your data room ready and respond promptly to requests.

Under pressure to close, sellers sometimes agree to warranties they can’t stand behind or that expose them to unreasonable liability. Review warranties carefully and push back where necessary.

Failing to disclose properly can leave you exposed to warranty claims. But over-disclosing or disclosing carelessly can also cause problems. Get the balance right with professional help.

Your involvement doesn’t end at completion. Earn-outs, handover periods, and warranty claims can all arise. Make sure the sale agreement protects your position during this period.

Choosing a law firm is a big decision. You want experts who actually get you and your business, respond when you need them, and give you straight answers. That’s us. We’re one of Wales’ leading commercial law firms, and we do things a little differently.

You won’t be passed through layers of gatekeepers here. When you call, you’ll speak to the solicitor handling your matter. You’ll have their mobile number, their email, and a genuine working relationship. Business sales move quickly, and you need advisers who are available when decisions need to be made.

We don’t work in silos. Our corporate team works closely with colleagues in employment and property to make sure every aspect of your sale is covered. If your deal involves TUPE, property assignments, or tax structuring, we’ll bring in the right people.

Devolved decision-making and flexible working hours mean we can move at pace. Deals have deadlines. Delays cost deals. We’re set up to respond when you need us, including outside regular office hours.

You’ll always get the full picture from us. If a buyer is asking for something unreasonable, we’ll tell you and help you push back. If there’s a risk you need to know about, we won’t sugar-coat it. Just practical guidance on what matters.

Selling your business should be about maximising what you get, not paying excessive legal fees. We’ll give you a clear fee estimate at the outset based on the transaction’s likely scope and complexity, and keep you updated as the matter progresses.

We’re the leading commercial law firm with offices in South and North Wales offering Welsh language legal services at every level, from trainees right through to partners. This isn’t an add-on or a tick-box exercise. It’s part of who we are.

We charge for business sale work based on the deal’s complexity and value:

Fixed fees – For smaller, straightforward sales, we can often agree a fixed price upfront.

Capped fees – For mid-sized deals with some variables, we may agree a fee cap so you have budget certainty.

Hourly rates – For larger or more complex sales, we charge by the hour but keep you regularly updated on costs. We will always endeavour to give you an estimate of our likely fees.

Contact us for a quote specific to your situation.

The support we had from the team at Darwin Gray meant that we were able to achieve what we needed without complication.

The typical process involves preparing your business for sale, finding a buyer (or engaging with buyers who’ve approached you), negotiating heads of terms, managing due diligence, negotiating and signing sale documentation, and completing the transaction. How long this takes depends on complexity, but expect 3-6 months from finding a buyer to completion. Starting preparation earlier makes the process smoother and often improves your outcome.

Tax depends on how the sale is structured, your personal circumstances, and whether you qualify for Business Asset Disposal Relief (BADR). Get specialist tax advice before committing to a structure, as the right approach can save significant amounts.

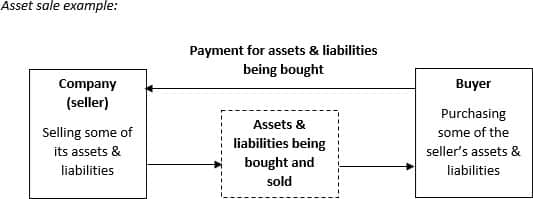

With an asset sale, a seller will only sell specific assets and liabilities which they agree with the buyer. This enables the seller to select only those aspects of the business that they want to sell. It also enables a buyer to exclude any liabilities that they don’t want to take over, and leave those with the seller.

After completion of the asset sale:

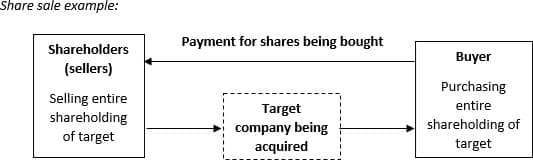

With a share sale, the seller will sell the target company “warts and all”. The buyer will purchase the entire shareholding of the company and therefore acquires all of its assets and all of its liabilities.

After completion of the share sale:

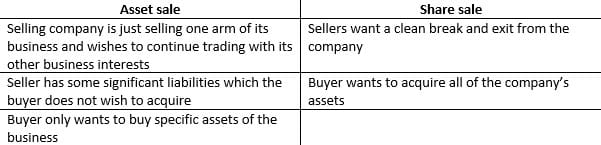

The circumstances of the business sale, and advice from professional advisers particularly surrounding tax issues, will usually dictate whether the sale of a business should be structured as an asset sale or a share sale. We would always advise prospective buyers and sellers of a business to take tax advice early on in the sale negotiations.

As a general starting point, here are some typical situations which would lean towards an asset sale and share sale:

Generally an asset sale is viewed as more buyer-friendly, and a share sale is viewed as more seller-friendly. The final decision on structure is likely to be determined by the negotiation power of both parties, and the tax advice received.

Business Asset Disposal Relief (formerly Entrepreneurs’ Relief) is a tax relief that reduces Capital Gains Tax on qualifying business disposals.

Timescales vary significantly. A straightforward sale to a known buyer might complete in 2-3 months. More complex deals typically take 4-6 months from heads of terms to completion. If you’re starting from scratch without a buyer, add time for finding one and initial negotiations. Factors affecting timing include the complexity of your business, how prepared you are for due diligence, how aligned buyer and seller are on terms, and whether any regulatory approvals are needed.

Due diligence is the buyer’s investigation of your business before they commit to buying. They’ll review financial records, contracts, employment arrangements, property, intellectual property, tax compliance, and other matters to understand what they’re buying and identify risks. As a seller, you’ll need to provide information and answer questions. Being well-prepared speeds up the process and reduces the chance of nasty surprises affecting the price.

Warranties are contractual statements about your business that you make in the sale agreement. They cover matters like the accuracy of accounts, ownership of assets, compliance with laws, and the state of contracts. If a warranty is untrue and the buyer suffers loss, they can claim damages. Warranties are standard in business sales because buyers need protection against things they couldn’t discover in due diligence. Your protection comes from negotiating reasonable warranties and making proper disclosures.

The disclosure letter qualifies the warranties in the sale agreement by setting out known exceptions. If you properly disclose an issue, the buyer can’t claim for breach of warranty on that point. Disclosure is your main protection against warranty claims. It needs to be thorough and accurate, covering everything the buyer should know that might otherwise breach a warranty. Getting disclosure right is a critical part of the sale process.

Several mechanisms protect sellers: negotiating reasonable warranties (pushing back on unreasonable ones), making thorough disclosures, agreeing liability caps and thresholds, setting time limits for claims, and excluding matters the buyer knew about. Warranty and indemnity insurance is also increasingly common, allowing risk to be transferred to insurers rather than sitting with the seller.

Restrictive covenants prevent you from competing with the business you’ve sold. Typically, they stop you setting up or working for a competing business, soliciting customers or employees, and using confidential information. Restrictions need to be reasonable in scope and duration to be enforceable. As a seller, you should negotiate the narrowest and shortest restrictions the buyer will accept, ensuring you can still earn a living and pursue future opportunities.

An earn-out is a payment mechanism where part of the purchase price depends on the business’s future performance. Earn-outs are used when buyer and seller disagree on value or when the seller is staying involved post-sale. While earn-outs can bridge valuation gaps, they’re also a common source of disputes. Clear drafting about how performance is measured and what happens if there’s disagreement is essential.

While there’s no legal requirement, professional advice is strongly recommended. Business sales involve significant legal complexity around deal structure, warranties, tax (including corporation tax), and ongoing liability. Buyers typically have professional advisers; without your own, you’re at a disadvantage. The cost of getting it wrong far exceeds the cost of proper advice. Experienced solicitors also help deals progress smoothly and protect your interests throughout.

Cardiff Office (Head Office)

9 Cathedral Road, Cardiff, CF11 9HA

Located in the heart of Cardiff’s business district, our head office is easily accessible by car and public transport. We advise business sellers across Wales and throughout the UK.

Bangor Office

Unit F12, InTec, Ffordd y Parc, Parc Menai, Bangor, LL57 4FG

Our North Wales office serves businesses across the region with the same expertise and direct access to our corporate team.

We advise on business sales throughout Wales and across the UK. Most of the transaction process can be handled remotely, so your location doesn’t limit our ability to help.

Whether you’re actively looking for a buyer, have received an approach, or just thinking about your exit options, we’re here to help you navigate the process and protect your interests.

Contact us for a free, no-obligation chat to see if we can help you. You’ll speak directly to a corporate solicitor who can discuss your situation and explain how we might work together.

If you need any advice on selling a business, please contact a member of our corporate and commercial law team in confidence here or on 02920 829 100 for a free initial call to see how they can help.

We aim to respond to all enquiries within one working day.

To speak to one of our experts today, please contact us on 02920 829 100 or by using our Contact Us form for a free initial chat to see how we can help.