Home Legal Services Company / Corporate

Expert legal advice for buying and selling shares in private companies across Wales and the UK.

Whether you’re selling your stake in a business you’ve built, buying shares from a departing shareholder, or acquiring a company outright, the share purchase agreement is the document that protects your interests. Get it right and the transaction runs smoothly. Get it wrong and you could be facing unexpected liabilities, tax problems, or costly disputes.

We help business owners, shareholders, and investors navigate share transactions with clear, practical advice. No unnecessary complexity, just straightforward guidance on what matters.

Get a free, no-obligation chat with our corporate and commercial team, call us on 02920 829 100 or use our Contact us form.

Excellent rating by Review Solicitors | Ranked in Legal 500 and Chambers & Partners.

Share transactions can feel daunting. There’s a lot at stake, plenty of legal jargon, and the process involves more steps than most people expect. But with the right solicitor in your corner, it doesn’t have to be stressful.

We act for buyers and sellers on share purchases of all sizes, from minority stake acquisitions to full company sales. Our corporate team has handled transactions ranging from straightforward share transfers between family members to complex deals involving multiple shareholders, deferred payments, and earn-out arrangements.

What you’ll get from us is honest advice about your position, clear explanations of what the documents mean, and practical support throughout the process. We’ll flag the issues that matter, help you negotiate terms that work, and make sure nothing falls through the cracks before completion.

If you’re thinking about buying or selling shares in a private company, let’s have a conversation about what’s involved.

Get a free, no-obligation chat with our corporate and commercial team, call us on 02920 829 100 or use our Contact us form.

A share purchase agreement (sometimes called an SPA or share sale agreement) is the contract that sets out the terms for buying or selling shares in a company. It’s the main legal document in any share transaction and covers everything from the purchase price to the protections each party needs.

Unlike buying business assets, when you buy shares you’re acquiring ownership of the company itself. The company continues with its existing contracts, employees, assets, and liabilities. The shares simply transfer from the seller to the buyer.

This makes the share purchase agreement particularly important. The buyer needs assurances about what they’re getting. The seller needs clarity on their ongoing obligations and protection against future claims. Both sides need certainty about when and how the deal completes.

A well-drafted SPA covers:

Every share transaction is different, so the agreement needs to reflect the specific circumstances of your deal. That’s where experienced legal advice makes a real difference.

Our share purchase agreement solicitors support both buyers and sellers through the entire transaction process. Here’s how we can help:

Selling shares, whether that’s your entire stake or part of it, involves significant decisions. You want to maximise your return while limiting your exposure to future claims.

We can help you with:

When you buy shares, you take on the company with all its history, including liabilities you might not know about. Proper due diligence and strong contractual protections are essential.

We can help you with:

Not all share transactions involve outside parties. Sometimes shareholders want to buy out a departing colleague, redistribute ownership within a family business, or reorganise their shareholdings.

We can help you with:

If you’re bringing in outside investors, the documentation needs to protect both the company and the new shareholders. Investment transactions often require additional agreements alongside the share purchase.

We can help you with:

Every transaction is different, but most share purchases follow a similar path. Here’s what typically happens:

Stage 1: Heads of Terms

Before diving into detailed legal documents, the parties usually agree on the basic commercial terms. This heads of terms document (sometimes called a letter of intent) sets out the price, structure, key conditions, and timeline. It’s mostly not legally binding, but it creates a roadmap for the deal and shows both sides are serious.

Stage 2: Due Diligence

The buyer investigates the target company to verify what they’re buying and identify any risks. This covers finances, contracts, employees, property, intellectual property, litigation, and regulatory compliance. The findings inform the negotiations and shape the protections needed in the SPA.

Stage 3: Drafting and Negotiation

The share purchase agreement is drafted, usually by the buyer’s solicitors. Expect several rounds of negotiation as both sides work through the warranties, limitations on liability, and other key terms. This is where experienced legal advice really counts, knowing which points to push on and which to concede can make or break a deal.

Stage 4: Disclosure

The seller prepares a disclosure letter setting out anything that qualifies the warranties in the SPA. If the seller has disclosed an issue, the buyer generally can’t claim for breach of warranty on that point. Getting disclosure right is critical for sellers.

Stage 5: Completion

Once all conditions are satisfied, the parties sign the SPA, transfer the shares, and exchange money. The buyer becomes the legal owner of the shares. There’s usually a bundle of completion documents including board minutes, stock transfer forms, and resignations of outgoing directors.

Stage 6: Post-Completion

After completion, there’s admin to handle: updating Companies House, stamping the stock transfer forms, notifying HMRC, and dealing with any completion accounts or earn-out calculations. We’ll make sure nothing gets missed.

Share purchase agreements contain a lot of legal terminology. Here’s a plain English guide to the provisions that matter most:

These are statements the seller makes about the company, for example, that the accounts are accurate, there’s no pending litigation, and all taxes have been paid. If a warranty turns out to be untrue, the buyer can claim for breach of contract. Sellers want to limit warranties; buyers want them to be as broad as possible.

An indemnity is a promise to reimburse the buyer pound-for-pound for a specific liability. Indemnities are typically used for identified risks that came up during due diligence.

The seller’s disclosure letter sets out exceptions to the warranties. If something is properly disclosed, the buyer can’t bring a claim for breach of warranty. Preparing this carefully is one of the most important jobs for the seller’s solicitor.

These cap the seller’s exposure under the warranties and indemnities. Common limitations include financial caps (often linked to the purchase price), time limits for bringing claims, minimum thresholds before claims can be made, and exclusions for matters disclosed or known to the buyer.

These are things that must happen before completion can take place, for example, regulatory approvals, third-party consents, or shareholder votes. The SPA sets out what happens if conditions aren’t satisfied by the target date.

These prevent the seller from competing with the business or poaching customers and employees after completion. They need to be reasonable in scope and duration to be enforceable.

Sometimes part of the price depends on the company’s financial position at completion or its future performance. Completion accounts adjust the price based on net assets or working capital. Earn-outs tie part of the consideration to hitting future targets.

When buying a business, you can either purchase the company’s shares or buy the business assets directly. Each approach has different implications.

Share purchase:

Asset purchase:

Which structure works best depends on your specific circumstances, the nature of the business, and what risks you’re willing to take on. We’ll help you think through the options and choose the right approach.

View more on buying a business

Choosing a law firm is a big decision. You want experts who actually get you and your organisation, respond when you need them, and give you straight answers. That’s us. We’re one of Wales’ leading commercial law firms, and we do things a little differently.

You won’t be passed through layers of gatekeepers here. When you call, you’ll speak to the solicitor handling your matter. You’ll have their direct dial, their email, and a genuine working relationship. Our clients tell us this makes all the difference, especially when deals move quickly and decisions need to be made.

We don’t work in silos. Our corporate team works closely with colleagues in employment and property to make sure every aspect of your transaction is covered. If your deal involves TUPE transfers or property issues, we’ll bring in the right people.

Devolved decision-making and flexible working hours mean we can move at pace. We’re set up to respond when you need us.

You’ll always get the full picture from us. Clear options, each with its own risk level, so you can make informed decisions. No sugar-coating, no hedging. Just practical, commercial guidance on what the documents mean and what you should push back on.

We know legal costs matter. We’ll give you a clear fee estimate at the outset and keep you updated as the transaction progresses. No nasty surprises at the end.

We’re the leading commercial law firm with offices in South and North Wales offering Welsh language legal services at every level, from trainees right through to partners. This isn’t an add-on or a tick-box exercise. It’s part of who we are.

We charge for share purchase work in different ways depending on the complexity:

Fixed fees – For straightforward share transfers between existing shareholders or simple purchases where the scope is clear, we can often agree a fixed price.

Capped fees – For standard transactions with some variables, we may agree a fee cap so you have budget certainty.

Hourly rates – For complex deals or where the scope is uncertain, we charge by the hour but keep you regularly updated on costs.

We’re always happy to discuss fees upfront. Contact us for a quote specific to your transaction.

They provide sensible and pragmatic advice. Legal 500![]()

They are flexible and responsive. Legal 500![]()

A share purchase agreement is the legal contract that governs the sale of shares in a company. It sets out what’s being sold, the price, when completion happens, and the protections each party receives. Unlike buying assets, when you buy shares you acquire the company itself with all its contracts, employees, assets, and liabilities. The SPA allocates risk between buyer and seller through warranties, indemnities, and other provisions. Getting these right is crucial because they determine who bears the cost if problems emerge after completion.

Start by deciding whether you want to sell all or some of your shares and who the buyer will be, whether that’s an existing shareholder, the company itself, an external investor, or a trade buyer. You’ll need to check your shareholder agreement and articles of association for any restrictions on share transfers. A solicitor will then help you negotiate terms, prepare or review the share purchase agreement, manage the disclosure process, and handle completion. The timeline depends on deal complexity.

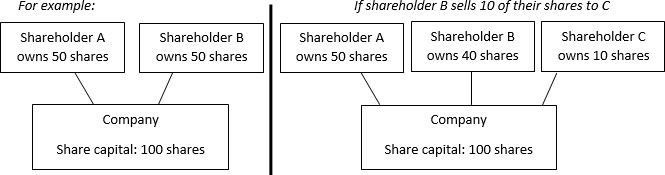

Buying and selling shares refers to an existing shareholder selling some or all of their shares in a company to another person. This might be between existing shareholders, or other people who are not already shareholders. The purchase price for the shares will be paid to the seller, and not to the company itself. The number of shares in issue does not increase.

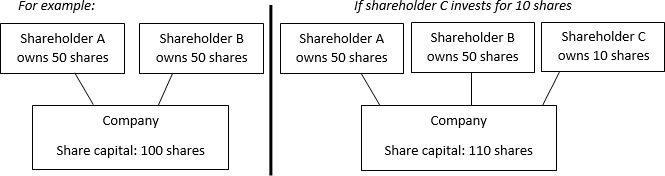

Investing in a business means agreeing to invest in the company itself in exchange for the allotment and issue of new shares in the company to the incoming shareholder. The investment money is paid to the company, and not to the existing shareholders. This also results in the share capital in the company being increased by the number of new shares issued.

The rest of this page will focus on purchasing shares from a shareholder.

You can transfer shares using just a stock transfer form, but for anything beyond a simple gift or nominal value transfer, legal advice is strongly recommended. Without a proper share purchase agreement, buyers have limited protection if things go wrong. Sellers risk ongoing liability without appropriate limitations. The legal costs are usually a small fraction of the transaction value, and the protection a well-drafted SPA provides is worth the investment. We’ve seen deals unravel and expensive disputes arise from poorly documented share transactions.

Due diligence typically covers corporate records, accounts, contracts, employees, property, intellectual property, litigation, and regulatory compliance. The scope depends on the deal size and the buyer’s existing knowledge of the company. For a full company acquisition from an external seller, you’d expect comprehensive due diligence. For a share purchase from a departing co-founder you’ve worked with for years, a lighter touch might be appropriate. The findings inform the warranties you need and may affect the price or deal structure.

Timescales vary significantly depending on complexity. A full company acquisition with extensive due diligence and negotiation typically takes 2-4 months, sometimes longer. Key factors include how quickly due diligence can be completed, whether the parties can agree terms, any regulatory approvals needed, and the availability of funding. We’ll give you a realistic timeline for your specific transaction and work to keep things moving efficiently.

Warranties are statements the seller makes about the company, such as the accounts being accurate, no undisclosed liabilities, and no pending litigation. If a warranty turns out to be untrue, the buyer can claim for breach of contract. Warranties shift risk from buyer to seller, so they’re heavily negotiated. Sellers want them narrow and capped; buyers want them as broad as possible. The disclosure letter qualifies the warranties by setting out known exceptions.

Yes, but you’ll need to check whether existing shareholders have pre-emption rights, meaning they get first refusal on any shares being sold. Most shareholder agreements and many articles of association include pre-emption provisions. These can be waived if the existing shareholders agree. If there’s no shareholder agreement, statutory pre-emption rights may apply to new share issues but not to transfers of existing shares. We’ll review the company’s documents and advise on the process.

If issues arise that breach the warranties in the SPA, the buyer may be able to claim compensation from the seller. The success of any claim depends on whether the issue was disclosed, whether any limitations on liability apply, and whether the claim is made within the time limits set out in the agreement. Indemnities provide pound-for-pound recovery for specific risks. Some deals use warranty and indemnity insurance to provide additional protection. Having a well-drafted SPA with appropriate protections is the best way to manage post-completion risk.

We act for both, though obviously not on the same transaction. Whether you’re buying or selling, our job is to protect your interests and get the deal over the line on terms that work for you. We’ll be upfront about what’s reasonable and where the negotiation points are, rather than taking aggressive positions that derail deals.

a: 9 Cathedral Road, Cardiff, CF11 9HA

Located in the heart of Cardiff’s business district, our head office is easily accessible by car and public transport.

a: Unit F12, InTec, Ffordd y Parc, Parc Menai, Bangor, LL57 4FG

Our North Wales office serves businesses across the region with the same expertise and direct access to our corporate team.

We advise clients throughout Wales and across the UK, meeting by video call or visiting your premises as needed.

Whether you’re selling shares in a business you’ve built, buying into a company, or reorganising ownership with existing shareholders, we’re here to help.

If you need any advice on buying and selling shares in a business, please contact a member of our corporate and commercial law team in confidence here or on 02920 829 100 for a free initial call to see how they can help.

To speak to one of our experts today, please contact us on 02920 829 100 or by using our Contact Us form for a free initial chat to see how we can help.